Government under financial pressure!

Government under financial pressure!

The government is under intensifying financial strain as revenue collection continues to lag behind targets, widening the budget deficit.

Disbursements from the International Monetary Fund have also been delayed due to unmet conditions, further limiting fiscal flexibility.

To bridge the gap, the government is increasingly turning to borrowing. It has already taken a record amount of loans from the banking sector and is seeking over $3.25 billion in fresh funds from development partners. At the same time, rising global fuel prices have eroded its ability to maintain subsidised domestic rates, forcing price hikes in the local market.

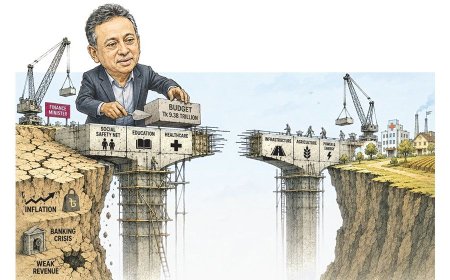

Despite weak revenue inflows, the government is preparing an ambitious budget for the next fiscal year. Spending pressures remain unavoidable, particularly due to rising debt servicing obligations at home and abroad. Available data suggests the state is operating under constraints similar to those of a financially stretched middle-income household.

According to the National Board of Revenue, the revenue shortfall in the first eight months of the fiscal year reached Tk71,472 crore. Of the Tk325,802 crore target, only Tk254,330 crore has been collected—about 22 percent below expectations. Meeting the annual goal now appears unrealistic, as monthly collections would need to exceed Tk75,000 crore, far above the current pace of under Tk40,000 crore.

All major revenue streams—income tax, VAT and import duties—have underperformed, with income tax showing the largest gap. Structural weaknesses persist, as only 4.6 million of roughly 12.8 million TIN holders have submitted returns. Sluggish imports and weak economic activity have also dragged down VAT collections.

Meanwhile, expenditure remains elevated, covering public sector salaries, infrastructure projects and other essential outlays, even amid austerity efforts. With revenues falling short, reliance on bank borrowing has surged.

Data from Bangladesh Bank shows government borrowing from banks has climbed to nearly Tk109,000 crore in just nine months—already exceeding the full-year target. Economists warn that such heavy borrowing could crowd out private sector credit, dampen investment and slow overall economic growth.

External debt is also rising. According to the Economic Relations Division, total foreign debt has surpassed Tk23,00,000 crore, with an additional $3 billion in new loans being sought. Repayment pressures are mounting, with about $26 billion due over the next five years.

Although Bangladesh secured a $4.75 billion programme from the IMF, uncertainty remains over future instalments due to unmet reform conditions. Recent discussions in Washington did not guarantee the release of the next tranche, raising concerns about budget execution.

Amid these pressures, the government has begun adjusting fuel prices. While initially reluctant, rising global costs and IMF-backed subsidy reforms have made price increases difficult to avoid. While this may ease fiscal pressure, economists caution it could also accelerate inflation.

The government is now planning a budget exceeding Tk925,000 crore for FY2026–27, driven by election commitments, expanded social safety nets, a new pay structure and higher subsidies. However, with revenue growth lagging, the budget deficit could approach 5 percent of GDP, heightening macroeconomic risks.

A growing portion of expenditure is being absorbed by interest payments and subsidies. Around Tk122,000 crore has been allocated for interest payments this fiscal year, with further increases expected. Subsidy demands—especially in the energy sector—continue to rise alongside development spending.

Business leaders and economists warn that without corrective measures, the country risks slipping into a debt trap. They emphasise the need to strengthen revenue mobilisation, modernise the tax system, curb evasion and improve the investment climate. Careful prioritisation of development spending is also critical.

Mohammad Hatem, president of the Bangladesh Knitwear Manufacturers and Exporters Association, cautioned that excessive reliance on bank borrowing could harm the economy and complicate future debt repayment.

Mustafizur Rahman of the Centre for Policy Dialogue stressed that avoiding a debt trap should be the government’s top priority, underscoring the importance of boosting revenue alongside borrowing.

Zahid Hussain, former lead economist at the World Bank’s Dhaka office, noted that while demand for long-term, low-cost financing is increasing, borrowing alone cannot resolve the crisis. He highlighted mounting macroeconomic pressures, including balance of payments risks, rising import costs, weak export earnings and uncertainties around remittance inflows—calling for coordinated reforms and sustained external support.

What's Your Reaction?