Market-based wealth tax: Can it raise revenue, or will it drive capital flight and increase harassment?

Concerns mount over increasing pressure on farmers and the middle class

Ahead of the national budget for FY2026–27, Bangladesh’s tax policy appears set for significant changes, according to signals from the National Board of Revenue (NBR).

Amid heated debate over a possible inheritance tax, NBR Chairman Md Abdur Rahman Khan has clarified that there is no current plan to introduce such a levy. However, he confirmed that the authority is actively developing a modern, technology-driven, database-based wealth tax system—an initiative that has already sparked concern among stakeholders.

Finance Division documents show the government is targeting a Tk9.30 lakh crore budget for FY27, with the NBR tasked to collect Tk6.95 lakh crore in revenue.

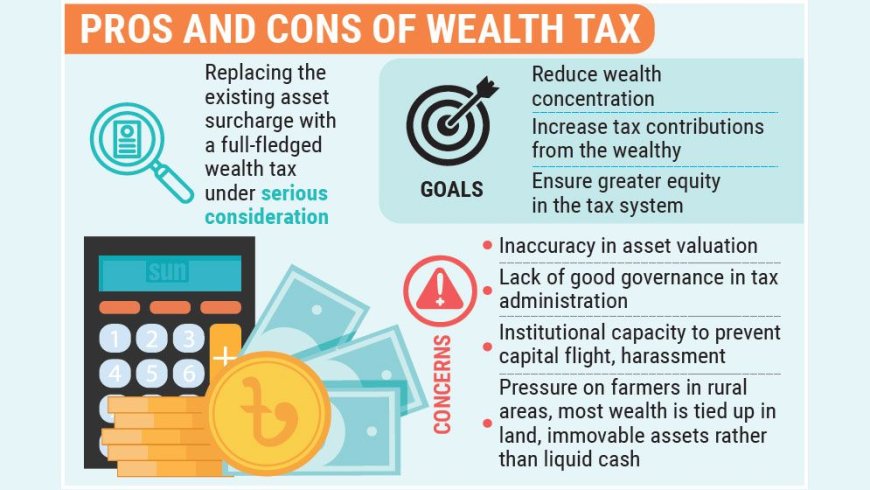

To meet this ambitious target, the NBR is pursuing major structural reforms aimed at expanding direct taxation and strengthening tax administration. Among the key proposals under discussion are replacing the existing asset surcharge with a comprehensive wealth tax and, until recently, the possible introduction of an inheritance tax.

Following strong criticism, the NBR chief has ruled out an inheritance tax for the upcoming fiscal year. Still, plans to introduce a wealth tax by scrapping the current surcharge system remain on track. The government is also considering valuing land and immovable assets based on market prices or mouza rates instead of deed values. A draft Wealth Tax Act has already been prepared and may be incorporated into the budget, subject to high-level approval.

According to the NBR chairman, the reforms aim to curb wealth concentration, increase contributions from high-net-worth individuals, and promote greater equity in the tax system. Under the proposed framework, taxpayers’ asset data would be integrated into a central database, with wealth tax returns linked to e-filing systems.

While experts generally consider wealth taxation fair in principle, they stress that accurate asset valuation, sound governance, and stronger institutional capacity will be essential to prevent capital flight and administrative harassment.

A major concern is how such a system would operate in Bangladesh’s economic context, particularly in a largely rural, agriculture-based society. With most wealth tied up in land and immovable assets rather than liquid income, taxing assets at market value could pose serious challenges for marginal farmers.

Critics note that land ownership does not necessarily translate into cash flow. Many individuals may appear asset-rich on paper but struggle with liquidity due to high production costs, market volatility, climate risks, and rising labour expenses. In such cases, implementing wealth tax could impose undue pressure, especially on farmers and low-income groups outside the formal tax net.

Enforcement also presents a major hurdle. Bangladesh’s economy relies heavily on informal sectors, and low tax compliance could make it difficult to impose such taxes effectively on average citizens, likely triggering resistance.

Shift from surcharge to wealth tax

Under the current income tax regime, individuals with net assets exceeding Tk4 crore are subject to a surcharge. Additional surcharges apply to ownership of multiple vehicles or large residential properties. The surcharge rate increases progressively—10% for assets between Tk4–10 crore, 20% for Tk10–20 crore, 30% for Tk20–50 crore, and 35% for assets above Tk50 crore. However, this is calculated on income tax payable, not directly on total assets.

For instance, someone with Tk5 crore in assets who pays Tk1 lakh in income tax would incur a 10% surcharge, or Tk10,000.

NBR data shows Tk296 crore was collected from surcharges up to February of the current fiscal year. Under the proposed system, taxation would shift directly to asset values. Suggested rates include 0.5% for assets between Tk4–10 crore, 1% for Tk10–20 crore, 1.5% for Tk20–50 crore, and 2% for assets above Tk50 crore, with valuations based on market or mouza rates.

A key safeguard is that wealth tax liability would not exceed the taxpayer’s income tax payable.

Economists broadly agree that taxing wealth aligns with welfare state principles. Dr M Masrur Reaz of Policy Exchange Bangladesh supports the concept, noting that those with greater wealth should bear a larger burden, but warns that weak valuation systems could encourage concealment and expand the shadow economy.

Dr Mustafizur Rahman of the Centre for Policy Dialogue adds that while such taxes are common in developed economies, careful design is crucial. Unrealistic rates or thresholds could undermine effectiveness.

Ground realities raise concerns

Despite theoretical support, serious implementation concerns remain, particularly in rural areas where wealth is largely non-liquid.

Former World Bank economist Zahid Hussain highlights the “asset-rich but cash-poor” dilemma, warning that many landowners may lack the liquidity needed to meet tax obligations. This is especially true in agriculture, where incomes fluctuate due to costs, market instability, and climate shocks.

Critics argue that taxing based on market value could disproportionately burden marginal farmers. Former secretary Mizanur Rahman raises concerns about retirees and low-income individuals, noting that additional taxes could force asset sales, leaving them financially vulnerable.

Risk of evasion and capital flight

Enforcement challenges also loom large. Former NBR chairman Badiur Rahman notes that traditional revenue measures are losing effectiveness as taxpayers become more adept at evasion. While wealth tax is seen as a new avenue for revenue generation, its success will depend on robust asset verification and enforcement.

Without strong safeguards, experts warn, wealthy individuals may still evade taxes or shift assets abroad. Poorly designed wealth or inheritance taxes could also discourage investment, incentivise avoidance strategies, and even prompt relocation to lower-tax jurisdictions.

There is also concern that such taxes could force the sale of family businesses or farms, disrupting operations, reducing employment, and eroding long-term economic value.

Structural constraints

Bangladesh’s broader tax structure presents additional challenges. With a tax-to-GDP ratio of just 7.1% in FY24—among the lowest in the region—experts argue that improving compliance and administrative capacity should take priority before introducing complex taxes like wealth or inheritance tax.

Globally, inheritance tax regimes vary widely. Countries like Japan and South Korea impose rates as high as 55% and 50%, while others—including Singapore, Malaysia, and Indonesia—have abolished or do not impose such taxes. In South Asia, Bangladesh, India, Pakistan, Sri Lanka, and Nepal currently have no formal inheritance tax, though debates continue.

In advanced economies such as the United States, United Kingdom, Canada, and France, wealth and estate taxes contribute around 2% of GDP, supported by strong institutions and high compliance levels—conditions that Bangladesh has yet to fully develop.

What's Your Reaction?