New Governor Faces Tough Challenge

New Governor Faces Tough Challenge

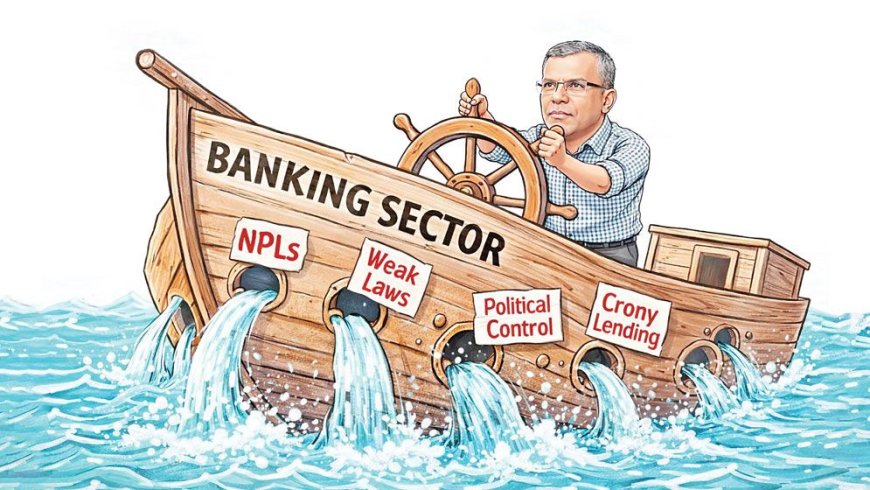

The new governor of Bangladesh Bank has taken office at a time when the country’s banking sector is mired in deep crisis, with record non-performing loans (NPLs), capital deficits and declining depositor confidence.

Economists and senior bankers caution that incremental administrative fixes will not suffice. They argue that the gravity of the situation now requires sweeping legal reforms, stronger governance standards and greater operational independence for the central bank.

By September 2025, total NPLs had soared to Tk6.44 lakh crore, representing nearly 36% of all outstanding loans—more than double the roughly 17% recorded a year earlier. In several banks, bad loans account for 60% to 70% of portfolios, effectively paralysing operations.

Amid this turmoil, five troubled Shariah-based banks—First Security Islami Bank, Social Islami Bank, Union Bank, Global Islami Bank and EXIM Bank—have been consolidated into a single entity, Sammilito Islami Bank PLC. The merged institution holds deposits of Tk1.31 lakh crore and serves more than 7.5 million customers. Successfully managing this merger and restoring public trust will be one of the new governor’s first major tests under the new government.

Meanwhile, the cancellation process for nine non-bank financial institutions is ongoing. To date, the interim government has enacted only two banking-related ordinances—the Bank Resolution Ordinance and the Deposit Insurance Ordinance—while broader reform initiatives remain stalled.

Officials at Bangladesh Bank say proposed amendments to the Bangladesh Bank Order, 1972 and the Bank Company Act have been held up at the finance ministry.

According to central bank sources, a revised draft amendment to the Bangladesh Bank Order—aimed at strengthening regulatory autonomy—has been awaiting approval for over four months. The initial proposal sought to remove three government officials from the central bank’s board. Following objections from the finance ministry, the draft was revised to retain one bureaucrat instead of three. It also proposes granting the governor ministerial rank and requiring the oath of office to be administered by the chief justice. Despite these revisions, clearance has yet to be granted.

A second major reform package concerns amendments to the Bank Company Act. Approved by the Bangladesh Bank board in October last year and later submitted to the finance ministry, the draft outlines 45 proposed changes.

Key measures include reducing the maximum size of bank boards from 20 directors to 15 and requiring independent directors to comprise at least half of the board—up from the current minimum of three. It also proposes that independent directors be selected from a vetted shortlist prepared by an expert committee.

Another notable provision aims to limit ownership concentration by preventing any individual, family or institution from holding more than a 5% stake in multiple banks.

Bangladesh Bank maintains that these reforms are essential to strengthening governance and oversight across both private and state-owned banks. However, resistance from the private sector has been strong. The Bangladesh Association of Banks has formally objected to the finance ministry, particularly regarding the proposed ownership cap.

The broader economic environment remains fragile. Inflation has persisted above 8%, while lending rates of 14%–15%—with the policy rate at 10%—have weighed on private investment. Liquidity strains at several banks have further heightened depositor anxiety.

Dr Zahid Hussain, former lead economist at the World Bank’s Dhaka office, questioned the prolonged delay.

“This is not a new file,” he noted, pointing out that the draft laws were prepared through extensive consultations involving the finance ministry, Bangladesh Bank and other stakeholders. He added that the reforms were reflected in mission reports of the International Monetary Fund and incorporated into the government’s Letter of Economic and Financial Policies, signed by both the finance minister and the Bangladesh Bank governor.

“After that process, the role of the finance ministry is straightforward—review the draft, clear it, or clearly explain why it cannot be cleared,” he said, adding that leaving the file pending for months inevitably raises concerns.

Dr Zahid suggested the delay may be driven more by questions of authority than by technical disagreements. “One key element of the reform is reducing the finance ministry’s representation on the Bangladesh Bank board. From that perspective, the issue is control,” he observed.

He stressed that central bank independence should not be viewed narrowly. “It is not only about fiscal dominance. It also involves bureaucratic dominance and influence from business lobbies.”

Dr Mustafa K Mujeri, a distinguished economist and former chief economist of Bangladesh Bank, emphasised that the new government must act swiftly to finalise legal reforms, reinforce regulatory autonomy, enhance transparency, publish forensic audit findings and hold financial offenders accountable.

“Without decisive steps,” he warned, “structural weaknesses in the banking sector could continue to undermine financial stability and delay broader economic recovery.”

What's Your Reaction?