Business Confidence Shaken as Interest Rates Rise, Investment Stalls

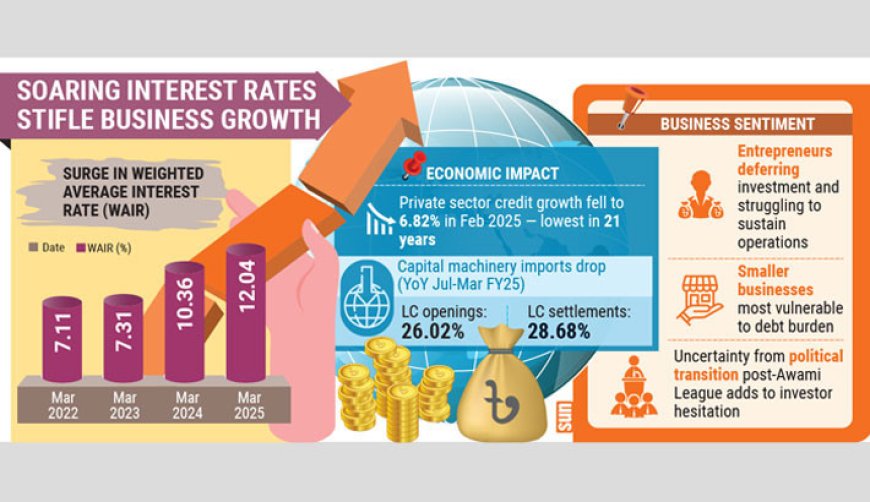

Weighted Average Bank Loan Rate Surpasses 12%

High interest rates, limited access to affordable financing, and ongoing political instability are squeezing businesses of all sizes—from start-ups and SMEs to large corporations—curbing their ability to invest in infrastructure, upgrade technology, or scale operations.

This financial pressure is eroding competitiveness, stalling innovation, and weakening job creation, business leaders warn.

According to Bangladesh Bank data, the weighted average interest rate on loans climbed from 7.11% in March 2022 to 7.31% in 2023, surged to 10.36% in 2024, and reached 12.04% by March 2025—marking a 4.93 percentage point jump over four years.

This average excludes additional charges banks often impose, which can push effective borrowing rates above 16%–17% in certain sectors.

The rapid rise in lending rates is discouraging new investment, with many firms unwilling to take on fresh debt amid rising financial stress. Private sector credit growth has plummeted to a 21-year low, dipping to just 6.82% in February 2025.

Small and medium-sized enterprises are particularly vulnerable, often unable to sustain high debt burdens, while larger firms are postponing capital spending. As a result, industrial growth is stalling and economic momentum is slowing.

Masrur Reaz, chairman of Policy Exchange Bangladesh, described the drop in capital machinery imports and credit growth as deeply concerning for a private sector-driven economy. He said investors are putting expansion plans on hold, driven by inflation-induced demand erosion and political uncertainty following the fall of the Awami League government last August.

Investor confidence remains fragile amid an unclear transition to democratic governance. Without greater stability, Reaz warned, long-term investment will remain subdued.

Shams Mahmud, president of the Bangladesh Thai Chamber of Commerce and Industry, echoed these concerns, citing high interest rates and a volatile business environment as major deterrents to new investment.

“The steep rise in interest rates is already slowing business expansion,” he told the Daily Sun. “As Bangladesh moves toward developing country status, affordable financing is crucial—but at these rates, businesses are holding back.”

Anwar-ul-Alam Chowdhury Parvez, president of the Bangladesh Chamber of Industries (BCI), linked the fall in capital machinery imports to persistent uncertainty. “Law and order have not improved, power supply is unstable, and interest rates have jumped from 9% to 16%—none of this inspires confidence,” he said. Entrepreneurs, he added, are now focused on survival, not growth.

Borrowing costs rise across sectors

Lending rates have risen steadily across all industries over the past year. Bangladesh Bank figures show that the weighted average interest rate (WAIR) on loans to large industries increased from 10.35% in March 2024 to 12.42% by March 2025. The SME sector saw a similar climb—from 10.51% to 12.43%—while agriculture loans rose from 10.75% to 11.83%.

With banks layering additional charges onto base rates, effective interest often exceeds 16%–17%.

Among individual banks, the National Bank of Pakistan posted the highest lending rate at 16.60%, followed by Global Islami Bank (16.36%) and Padma Bank (16.11%). Others with elevated WAIRs include Citizens Bank PLC (15.20%), National Bank (15.01%), and ICB Islamic Bank (14.69%).

The Bangladesh Bank had capped lending rates at 9% in April 2020. But to address post-COVID and global economic turbulence, it introduced a market-linked SMART rate in June 2023, pegged to treasury bill yields. In May 2024, it reverted to a fully market-driven system, giving banks more flexibility to set rates based on client risk profiles, loan demand, and liquidity.

Capital machinery imports plunge by 26%

The slowdown in industrial investment is reflected in import data. In the July–March period of FY2024–25, letters of credit (LCs) opened for capital machinery dropped by 26.02% year-on-year. LC settlements declined even more sharply, by 28.68%.

While LC openings for consumer goods rose ahead of Eid, activity in other categories dropped: intermediate goods fell by 1.61% (with settlements down 7.51%), and petroleum LCs declined by 3.83%.

What's Your Reaction?