All loans and advances will be classified if they remain overdue for more than three months

All loans and advances will be classified if they remain overdue for more than three months

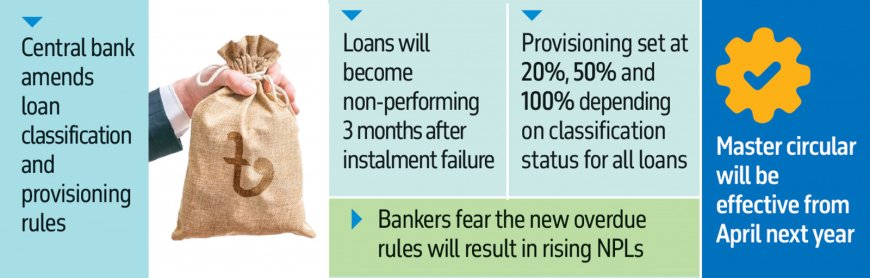

Under a master plan designed to improve risk management and financial transparency, all loans and advances will be classified if they are overdue for more than three months.

On Wednesday, Bangladesh Bank (BB) issued a new master circular on loan classification and provisioning, updating the rules for all banks and lending institutions.

The circular outlines the central bank's plan to implement an Expected Credit Loss (ECL) provisioning system by 2027, in line with International Financial Reporting Standard (IFRS 9). This move, which will be effective from April next year, will fully align Bangladesh’s loan classification and provisioning process with BASEL-III standards.

The circular, issued by the Banking Regulations and Policy Department (BRPD) of BB, divides loans and advances into four categories for classification: (a) Continuous Loan, (b) Demand Loan, (c) Fixed-term Loan, and (d) Short-term Agricultural Credit. Loans will be considered overdue from the day after their due date or upon creation of a forced loan if not repaid or renewed.

For Fixed-term Loans, any unpaid installment(s) will be classified as overdue from the day after the expiry or due date.

Loans will be classified into six categories: Standard-0 (STD-0), Standard-1 (STD-1), Standard-2 (STD-2), Special Mention Account (SMA), Sub-Standard (SS), and Doubtful (DF). Loans overdue for more than three months but less than six months will be classified as 'Substandard,' while loans overdue between six and 12 months will be 'Doubtful.' Loans overdue for more than 12 months will be classified as 'Bad.'

The classification should reflect the borrower’s deteriorating creditworthiness and the expected impact on repayment, according to the central bank.

A loan can be reclassified to a more favorable category if the overdue amounts are repaid in accordance with the original agreement. If a loan is classified based on the bank's qualitative judgment, it can be moved to a better category with justification showing improvements in payment or the borrower's financial condition.

Loans classified during Bangladesh Bank's inspection cannot be declassified without approval from the Department of Banking Inspection.

Regarding provisions, banks are required to maintain 1% of outstanding loans for STD-0, STD-1, and STD-2, 5% for SMA, and specific provisions of 20% for SS, 50% for DF, and 100% for loans classified as 'Bad.' These are the minimum provisions, and banks are encouraged to assess the adequacy of provisions continuously.

The circular also applies to Islamic banks for their investments.

Mohammad Shahriar Siddiqui, BB's director (BRPD), confirmed that all loans, including those in agriculture and terms, will be classified once overdue for more than three months.

Md. Touhidul Alam Khan, Managing Director & CEO of National Bank Limited (NBL), praised the timely introduction of the ECL framework and the new loan classification system, which he believes will align Bangladesh’s banking system with international standards and enhance the stability and resilience of financial institutions.

What's Your Reaction?