Investors may end up with nothing from NBFI liquidation efforts

Investors may end up with nothing from NBFI liquidation efforts

Investors are unlikely to recover any value from their holdings in the non-bank financial institutions (NBFIs) now slated for liquidation under a Bangladesh Bank initiative.

In a first-of-its-kind large-scale move, the central bank has decided to wind up nine out of the country’s 35 NBFIs in an effort to safeguard depositors and restore confidence in the financial sector.

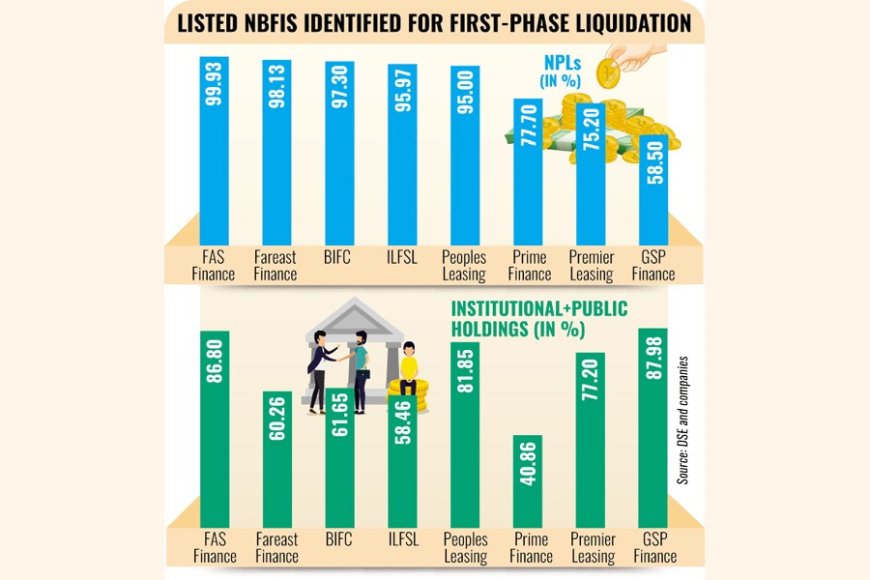

Of these nine, eight are listed on the stock exchanges: FAS Finance and Investment, Bangladesh Industrial Finance Company, Premier Leasing and Finance, Fareast Finance and Investment, GSP Finance, Prime Finance, People’s Leasing and Financial Services, and International Leasing and Financial Services.

Years of irregularities, loan scams, and mismanagement under the previous government crippled these institutions, leaving them unable to repay depositors. Several directors were accused of massive embezzlement, deepening public mistrust in the sector.

According to Dhaka Stock Exchange data, public and institutional investors currently hold between 40.86% and 86.8% stakes in these companies. But analysts say the chances of recovering any of that money are negligible. High levels of defaulted loans, negative capital, ballooning liabilities, and prolonged losses have left the firms insolvent.

“Ordinary investors should not expect anything, as they will be last in line when dues are settled,” said Akramul Alam, head of research at Royal Capital.

Under liquidation rules, payments go first to external creditors, then depositors, debenture holders, and preferential shareholders. Ordinary shareholders are the last priority.

Most of the nine NBFIs are effectively bankrupt, with up to 99.9% of their investments classified. Their non-performing loan ratios range from 58.5% to 99.9%, creating huge equity shortfalls.

“Liquidation means shutting down operations and selling off assets to repay obligations,” explained Md Sajedul Islam, managing director of Shyamol Equity Management. “If they cannot repay depositors, there is no way general shareholders will get their money back.” He added that only government action to sell sponsor-directors’ personal assets could provide investors with some relief.

Mr. Islam also urged accountability for those behind the collapse. “We’ve been warning about this for years. Timely intervention could have prevented much of the damage,” he said.

The Bangladesh Securities and Exchange Commission (BSEC) has not yet been formally informed of the liquidation plan. “We will try to safeguard general investors’ interests once the central bank notifies us,” said Abul Kalam, the BSEC spokesperson, though he declined to say whether shareholders could recover funds.

Meanwhile, investors have already begun dumping NBFI stocks. Last week, shares of the affected firms were among the biggest losers on the Dhaka Stock Exchange, plunging between 19% and 33%. Most now trade at well below their face value of Tk 10, with some priced under Tk 2.

Bangladesh Bank Governor Dr. Ahsan H Mansur assured depositors that their funds would be protected but stressed that sponsor-directors must face consequences. “We are taking this step solely to protect depositors,” he said.

The liquidation will be carried out under the Finance Company Act 2023. The central bank will apply to the High Court for approval, after which liquidators will be appointed. The regulator estimates the process could cost Tk 80–90 billion but sees it as essential to “clean up the industry.”

Earlier this year, Bangladesh Bank identified 20 weak NBFIs and issued show-cause notices. Nine were ultimately marked for liquidation after failing to provide satisfactory responses.

The problems, however, are long-standing. Chronic governance failures and unchecked irregularities hollowed out the sector. A notorious case is that of Prashanta Kumar Halder, former managing director of Reliance Finance and NRB Global Bank, who siphoned more than Tk 35 billion from four NBFIs—People’s Leasing, International Leasing, FAS Finance, and BIFC—using forged documents.

What's Your Reaction?