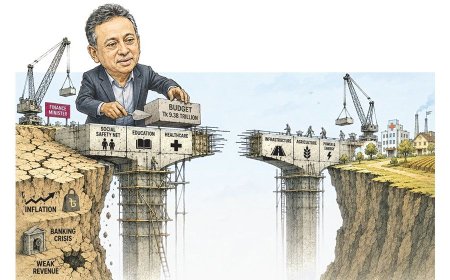

Industries face a multitude of challenges

Rising bank loans, a continuous shortage of dollars, escalating energy scarcity due to higher fuel costs, and growing wages have compelled production units to run at significantly reduced capacity.

Bangladesh's major industrial conglomerates are facing significant difficulties in navigating an increasingly challenging business environment, worsened by repeated shocks over the past few years, according to industry insiders.

Key issues such as growing bank loans, a persistent dollar shortage, escalating energy shortages amid higher fuel prices, and rising wages have forced production units to operate well below capacity, they noted.

The situation has deteriorated since the fall of Sheikh Hasina on August 5, with labor unrest and public order breakdown further destabilizing the industrial sector.

Private sector leaders are warning that the ongoing crises threaten the livelihoods of millions of workers and place the country's industries, businesses, and investments under immense pressure.

Although Bangladesh's broader economy weathered the COVID-19 pandemic relatively well, it has struggled to cope with global disruptions caused by the Ukraine war.

A continued shortage of dollars, exacerbated by sanctions and counter-sanctions between Russia and the West, has significantly impacted critical imports.

In May 2022, the exchange rate stood at Tk86, but it has now risen to Tk120.

This shortage has limited the import of raw materials for the garment sector and other industries, while increasing costs for even the most basic production activities, eroding working capital.

The energy crisis, which predates the Ukraine war and was made worse by repeated price hikes under the previous administration, remains another major obstacle.

Industries Facing Multiple Challenges

Ha-Meem Group Managing Director AK Azad recently pointed out that electricity costs nearly doubled under the Awami League government, yet industries are still facing daily power outages of 5–6 hours. This energy and fuel crisis has led most factories to operate at only 30–50% of their capacity.

The situation worsened following a post-Hasina crackdown on crony capitalists and bank loan defaulters, which some business leaders have criticized as "politically motivated."

They argue that such actions could further impede industrial growth during an already fragile period.

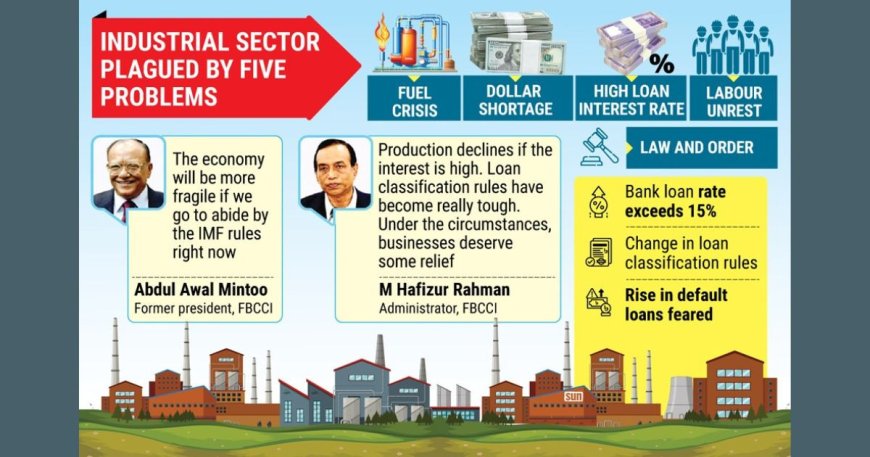

New loan classification regulations have increased the likelihood of defaults, and higher interest rates, aimed at controlling inflation, have discouraged business investments.

BNP leader and businessman Abdul Awal Mintoo, speaking to Kaler Kantho, alleged that widespread misuse of bank loans during the 15-year Awami League regime was facilitated by corrupt pro-Awami League bank officials.

However, he described the crackdown on defaulters as untimely, warning that it is preventing companies from sustaining their operations.

Labor unrest, often attributed to alleged Indian conspiracies and pro-Awami League sabotage, has resulted in the closure of more than 50 garment factories since August 5. This turmoil has redirected significant import orders to India, reducing foreign purchasing orders by 20%.

The ready-made garment (RMG) and textile sectors—key drivers of Bangladesh’s economy—have been particularly hard-hit.

The Bangladesh Textile Mills Association (BTMA) reports that prolonged fuel and gas shortages have reduced production capacity to 40–50% for more than three years.

Federation of Bangladesh Chambers of Commerce and Industry (FBCCI) Administrator Md Hafizur Rahman stated that the business community has not yet reacted officially to the stricter measures against loan defaulters.

“However, the interest rate has indeed become high. If the interest rate is high, production comes down. It becomes difficult to invest. The terms of defaulted loans have also become harsher. This is a delicate time. As a result, business people could use some relief,” he said.

FBCCI former president Abdul Awal Mintoo also remarked, “The country’s economy may be fragile if we follow all rules of the International Monetary Fund (IMF) now.”

Millions of Jobs at Risk

Thermax Group, which operates 17 factories, has been running many of them at reduced capacity due to shortages of raw materials.

Despite these challenges, the company exported over Tk2,500 crore in 2022-23, employing 22,500 workers and incurring significant monthly expenses on wages (Tk28 crore) and utilities (Tk17 crore).

However, its debt, including compounded interest, has ballooned to Tk7,248 crore.

Fakir Fashion Ltd, a major garment exporter employing 50,000 workers, has faced legal and reputational issues, damaging its credibility with international buyers.

Noman Group, employing 80,000 workers and contributing $1.3 billion annually to exports, has reported political targeting that has disrupted its operations and eroded foreign buyer confidence.

In a letter, Managing Director Mohammad Abdullah Zubair stated, “We have been conducting business with hard work and honesty for a long time and are not involved in petty politics. But we have been targeted after the change in the political situation.”

RMG Exports Drop by 5.22% in FY24

The ready-made garment (RMG) sector, which contributes around 84% of Bangladesh’s total export earnings, is facing severe challenges.

With over 2,000 exporters and 4 million employees directly involved, the industry is dealing with a combination of political instability, labor unrest, letter of credit (LC) constraints, high lending rates, energy shortages, and banking sector disruptions.

Former BGMEA director Mohiuddin Rubel told Daily Sun, “The business community has not yet recovered from the impact of COVID. Since then, industries have been dealing with numerous challenges. Many factories are shutting down, and companies are struggling to survive. If the issue of bad loans is addressed strategically, it will benefit everyone.”

RMG exports dropped by 5.22% in FY24, falling from $38.14 billion in FY23 to $36.15 billion.

Rubel expressed hope for the future, stating, “Positive signs may emerge in 2025 if the business community receives solutions to policy gaps, banking issues, energy shortages, and political instability. These measures could drive both export and investment growth in the coming years.”

High Registration Costs Burden Real Estate Sector

Md Wahiduzzaman, president of the Real Estate and Housing Association of Bangladesh (REHAB), highlighted the significant role of the real estate sector in the country’s economy.

Speaking to Daily Sun, he noted that approximately 200 industries are connected to the real estate sector, employing nearly 5 million workers and contributing 15% to Bangladesh’s GDP.

“The industry faced significant challenges in 2024. Following the mass revolution, we are working to recover. However, high registration costs, increased VAT and taxes, and the delayed implementation of Asian Development Bank (ADB) programs due to the economic slowdown have further impacted our sector,” Wahiduzzaman explained.

He expressed optimism for the future, stating, “The industry can overcome these challenges in 2025 if we receive proper policy support from the government.”

What's Your Reaction?